Mains >

Economic Development > Indian Economy and issues > Banking sector

SYLLABUS

GS 3: Economic Development > Banking sector

REFERENCE NEWS

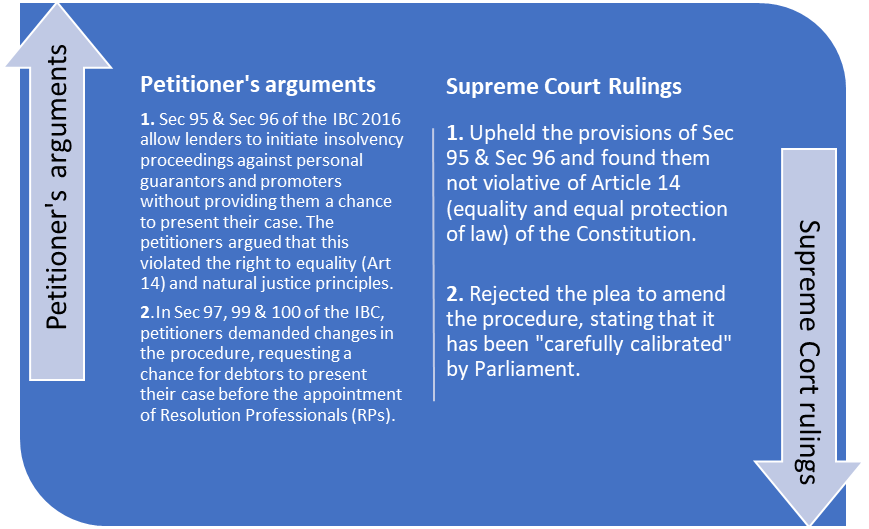

Recently, the Supreme Court delivered a significant ruling on the Insolvency and Bankruptcy Code (IBC) 2016, affirming key provisions and addressing various concerns raised by industrialists and promoters, including Anil Ambani, Venugopal Dhoot, Sanjay Singal, and Kishore Biyani.

ABOUT THE CASE

WHAT IS THE INSOLVENCY AND BANKRUPTCY CODE,2016?

The Insolvency and Bankruptcy Code was enacted in 2016, and it replaced all the existing laws with a uniform procedure to resolve insolvency and bankruptcy disputes. The code aimed to address the issue of Non-performing Assets (NPAs) and debt defaults.

Objectives

Consolidation and amendment of all existing insolvency laws in India.

Simplification and expedition of the Insolvency and Bankruptcy proceedings in India.

Protection of the interests of creditors and stakeholders in the company.

Reviving the company in a time-bound manner.

Framework

Insolvency Professionals: These professionals administer the resolution process and manage the debtor's assets while providing information for creditors.

Insolvency Professional Agencies: They register and certify insolvency professionals and enforce a code of conduct for their performance.

Information Utilities: These entities maintain records of creditor debts and repayments/dishonors to facilitate the insolvency process.

Adjudicating Authorities (NCLT and DRT): NCLT handles cases for companies and limited liability entities, while DRT handles cases for individuals and partnership firms.

Insolvency and Bankruptcy Board of India (IBBI): This board regulates insolvency professionals, agencies, and information utilities under the IBC.

Time Period for Insolvency Resolution: The IBC initially set a 180-day deadline for resolution, extendable by 90 days, but subsequent amendments allowed for a maximum period of 330 days, with possible extensions in exceptional cases.

Key Terms

Insolvency: It is a situation in which a debtor is unable to pay his/her debts.

Bankruptcy: It is a legal proceeding involving a person or business that is unable to repay their outstanding debts.

Liquidation: It is a process of bringing a business/company to an end. It involves the distribution of the company’s assets among creditors and other claimants.

Haircut: It refers to the reduction in the value of an asset. If the haircut is 50%, then the creditors will only get 50% of the amount that they loaned out.

Moral Hazard: It is a situation where an economic actor has an incentive to increase its exposure to risk because it does not bear the full costs of that risk.

SIGNIFICANCE OF IBC

Increase in the rate of recovery of the lenders/creditors- Lok Adalat, Debt Recovery Tribunal and SARFAESI Act, which were the recovery mechanisms available to lenders before enactment of the IBC, had a low average recovery of 23%. However, under the new IBC regime, the recoveries have risen to 43%.

Shift of focus to ‘Resolution’ rather than ‘liquidation’- IBC process aims to put the financially ailing corporate entities on their feet through a rehabilitation process. The primary focus has shifted to ‘saving rather than selling’.

Shift from ‘debtor-in-possession’ to ‘creditor-in-control’- The creditor-in-control model hands control of the debtor to its creditors and relies upon the managerial skills of a newly appointed management to take over an ailing company and ensure business continuance.

Improvement in India’s global rankings in resolving insolvency- An IMF-World Bank study in January 2018 observed that India is moving towards a new state-of-the-art bankruptcy regime. Since enactment of the Insolvency and Bankruptcy Code, India significantly improved its ‘Resolving Insolvency’ ranking to 108 in 2019 from 134 in 2014 , where it remained stagnant for several years. India won the Global Restructuring Review award for the most improved jurisdiction in 2018.

Stability of Indian financial systems- The SC in Swiss Ribbons Vs Union of India, has held that the core objective of the Insolvency and Bankruptcy Code, is to ensure revival and continuation of the corporate debtor. Insolvency and Bankruptcy Code is playing a larger role of public-welfare by ensuring the stability of Indian financial systems.

CHALLENGES WITH IBC

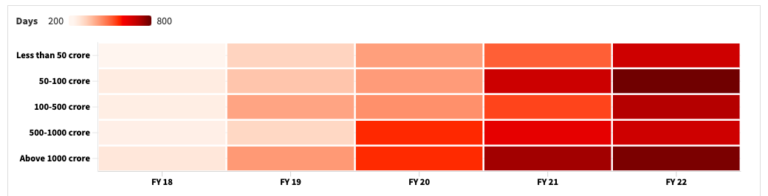

Delays in the resolution process- Resolution and liquidation cases have been taking longer than the mandated time of 330 days. For example- In cases of over Rs 1,000 Crore, the average resolution time has risen to 772 days in FY2022 from 274 days in FY2018.

Source- The Hindu. Shows the time taken for resolution processes to get completed

Greater liquidation than resolution- The objective of Insolvency and Bankruptcy Code, was to promote resolution, but it has ironically resulted in more liquidation. This hinders the economic potential of the country. A/c to IBBI, the number of cases seeing liquidation are three times more than that of resolution.

Big Haircuts- Longer delays in the IBC process, has resulted in larger haircuts, as the value of sick companies tends to diminish at an increasing pace over time. For instance- The lenders took a haircut of 83% in Alok Industries case, 90% Reliance Infratel case and 96% in the recent Videocon Group case.

Infrastructural Issues and Resource Deficit- Out of the 25 NCLT benches establlished across the country, most of these NCLT benches remain non-operational or partly operational, on account of lack of proper infrastructure or adequate support staff.

Fear of Vigilance inquires in case of govt lending institutions- The public sector banks fear risk-taking in a resolution process, as low rate of dues recovery in the short term, may subject them to vigilance inquiries and audits. Hence, these public lending institutions focus more on liquidation and safe exit.

Exclusion of promoters from the resolution process- There are many cases, where a loan default occur for reasons beyond the control of the promoters. However, IBC has strictly excluded the promoters from the resolution and liquidation process, despite the promoters not being wilful defaulters.

No focus on mediation, settlement and arbitration under IBC- Globally, a mechanism like the IBC’s corporate insolvency resolution process (CIRP) is used as a last-resort measure after all other alternatives like mediation, settlement and arbitration have been exhausted. However in India, there are no specific provisions for mediation under the IBC.

WAY FORWARD

Address the resource and infrastructure deficit in NCLT- The NCLT benches must be filled with competent financial professionals, who must use the Insolvency and Bankruptcy Code’s platform as a resolution tool instead of recovery tool.

Promotion of Alternative Dispute Redressal(ADR) Mechanism- The ADR mechanisms like mediation, arbitration and settlement must be explored first. The insolvency proceedings must be used as a last resort. The Mediation Act 2023 and the Arbitration Act 2021 are steps in the right direction.

Protecting the public sector bankers in case of bona-fide resolution decision- The ‘Business judgment’ rule that protects the board of directors in many countries for bona-fide decision-making must be introduced for public sector bank officials in India.

Allowing the defaulters who are not wilful ones to bid at NCLT- The defaulters who are not wilful defaulters and who have no hand in the failure of their business should be allowed to take part in the resolution and the liquidation process. For ex- many businesses failed due to COVID.

Proper use of National Asset Reconstruction comapny- The NARCL established by the government must be used in resolutions of companies which do not attract many strategic investors. Proper use of NARCL will help in increasing the resolutions and reduce the liquidations.

While the Insolvency and Bankruptcy Code (IBC) has shown promise, certain reforms like extending pre-packaged insolvency schemes beyond MSMEs is essential to unlock its full potential and provide a more comprehensive solution for distressed businesses across various sectors.

PRACTICE QUESTION

Q:"Discuss the impact of the Insolvency and Bankruptcy Code (IBC) on India's financial sector and its effectiveness in addressing the issue of non-performing assets (NPAs)."(15marks, 250 words)