Account Aggregator Network

2022 AUG 19

Preliminary >

Economic Development > Miscellaneous > Financial market

Why in news?

- Securities and Exchange Board of India (SEBI) officially joined the Account Aggregator (AA) framework, further strengthening the consent-based financial data sharing infrastructure.

More on news:

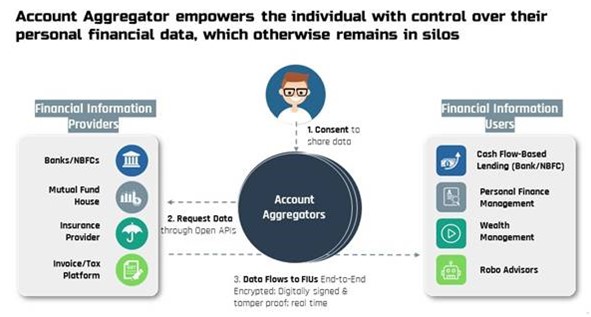

- Account Aggregator empowers the individual with control over their personal financial data, which otherwise remains in silos.

- This is the first step towards bringing open banking in India and empowering millions of customers to digitally access and share their financial data across institutions in a secure and efficient manner.

- The Account Aggregator system in banking has been started off with eight of the India’s largest banks. The Account Aggregator system can make lending and wealth management a lot faster and cheaper.

What is an Account Aggregator?

- An Account Aggregator (AA) is a type of RBI regulated entity (with an NBFC-AA license) that helps an individual securely and digitally access and share information from one financial institution they have an account with to any other regulated financial institution in the AA network.

- Data cannot be shared without the consent of the individual.

- There will be many Account Aggregators an individual can choose between.

- Account Aggregator replaces the long terms and conditions form of ‘blank cheque’ acceptance with a granular, step by step permission and control for each use of your data.

How will the new Account Aggregator network improve citizen’s financial life?

- India's financial system involves many hassles for consumers today - sharing physical signed and scanned copies of bank statements, running around to notarise or stamp documents, or having to share your personal username and password to give your financial history to a third party.

- The Account Aggregator network would replace all these with a simple, mobile-based, simple, and safe digital data access & sharing process.

- This will create opportunities for new kinds of services – example: new types of loans.

- The individual's bank just needs to join the Account Aggregator network

???????How is Account Aggregator different to Aadhaar eKYC data sharing or credit bureau data sharing?

- Aadhaar eKYC and CKYC only allow sharing of four ‘identity’ data fields for KYC purposes (eg name, address, gender, etc). Similarly, credit bureau data only shows loan history and/or a credit score.

- The Account Aggregator network allows sharing of transaction data or bank statements from savings/deposit/current accounts.

What kind of data can be shared?

- Today, banking transaction data is available to be shared across the banks that have gone live on the network.

- Gradually the AA framework will make all financial data available for sharing, including tax data, pensions data, securities data (mutual funds and brokerage), and insurance data will be available to consumers. It will also expand beyond the financial sector to allow healthcare and telecom data to be accessible to the individual via AA.

Is the data sharing secure?

- Account Aggregators cannot see the data; they merely take it from one financial institution to another based on an individual's direction and consent

- The data AAs share is encrypted by the sender and can be decrypted only by the recipient

PRACTICE QUESTION

With reference to ‘Account Aggregators’, consider the following statements:

1. They are regulated by Reserve Bank of India.

2. Sharing of banking transaction data through Account Aggregator network are prohibited in India.

Which of the statements given above is/are correct?

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Answer – A